Understanding the Legal Principles of Subrogation in Insurance: Your Friendly Guide!

Hey there, insurance adventurer! Ever wondered what happens after your insurance company swoops in to help you after a claim? You know, when they pay out for that fender bender or that leaky roof? Well, there’s a fascinating legal principle at play, and it’s called subrogation. Sounds a bit fancy, right? But don’t worry, I’m here to break it all down for you in a way that feels like we’re just chatting over coffee. We’ll uncover what subrogation really means, why it’s so important, and how it works behind the scenes. Ready to dive in? It’s a journey we’ll take together, making sure you feel completely in the loop!

- Subrogation is basically the right of your insurer to step into your shoes to recover damages from a third party who caused your loss.

- It ensures that the at-fault party is ultimately responsible for the damages, not just you or your insurer.

- This principle helps keep insurance premiums lower for everyone by recouping some of the claim costs.

- Understanding subrogation empowers you and clarifies the claims process.

What Exactly is Subrogation? Let’s Unpack It!

Think of subrogation as your insurance company’s superpower, allowing them to pursue the responsible party after they’ve paid your claim. It’s like they’re saying, “Okay, we helped our friend here, but now we’re going to go after the person who actually caused the mess!” This is a really crucial part of how the insurance world keeps things fair. It’s not just about you getting back on your feet; it’s also about making sure the person or entity that messed up is held accountable. This process, rooted deeply in contract law and insurance statutes, aims to prevent unjust enrichment, meaning no one gets paid twice for the same loss. Pretty neat, huh? It’s a system designed for fairness, and you’re a vital part of understanding it!

You

Suffered a loss and filed a claim.

Your Insurer

Steps in and pays your claim promptly.

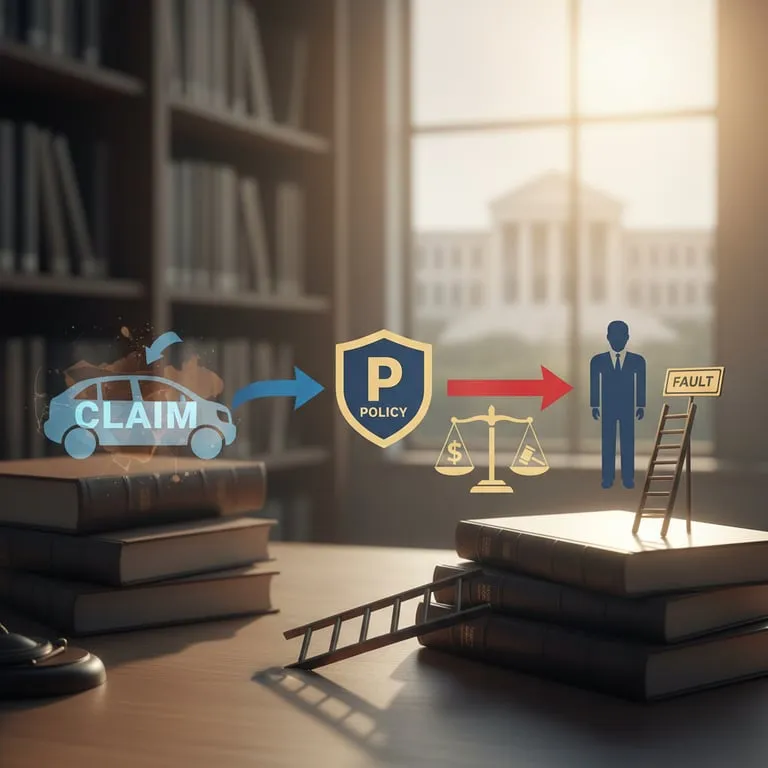

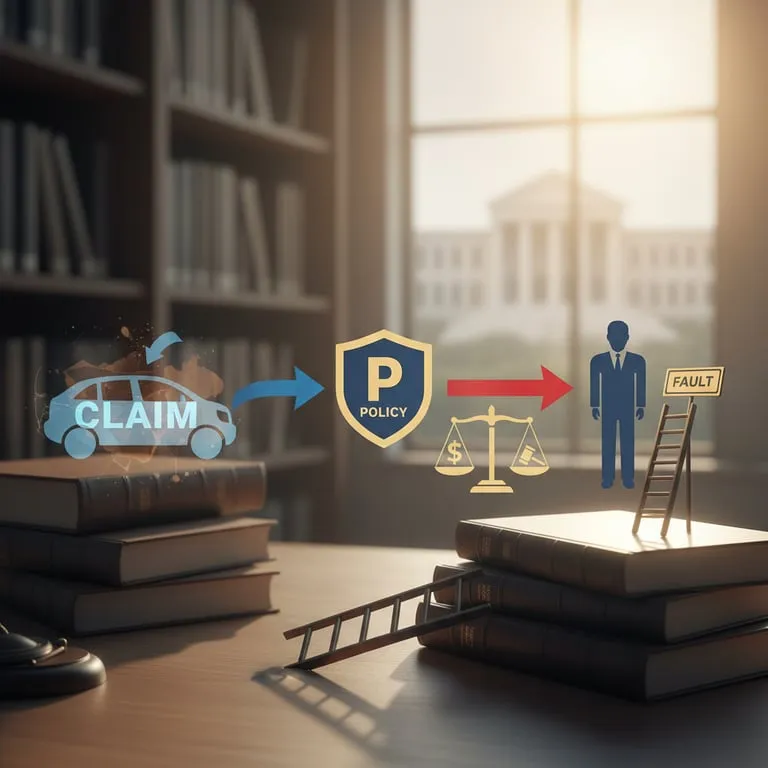

Subrogation in Action

Your insurer pursues the at-fault third party to recover their payout.

The “Why” Behind Subrogation

So, why do we even need subrogation? Well, it’s a cornerstone of fairness and affordability in insurance. Imagine this: a negligent driver runs a red light and crashes into your car. Your insurance company steps in, pays for your repairs, and gets you back on the road. Without subrogation, your insurer would essentially absorb that cost. But with it, they have the legal right to go after the negligent driver (or their insurance company!) to recover the money they paid out. This means the person truly at fault bears the financial burden, which is exactly how it should be! It also helps keep insurance premiums down for everyone. When insurers can recover some claim costs, it reduces their overall losses, which in turn can lead to more stable or even lower premiums for policyholders. Think of it as a collective effort to maintain a more affordable insurance market for all of us.

How Does Subrogation Actually Work? A Peek Behind the Curtain!

Let’s walk through a typical scenario. Suppose a faulty appliance in your rental unit causes a fire, damaging your belongings. You file a claim with your renter’s insurance, and they promptly pay you for the damaged items. Now, because of the subrogation clause in your policy, your insurance company has the right to pursue the appliance manufacturer or even the landlord (if they were negligent in maintenance) to recover those costs. This often involves investigation, demand letters, and sometimes, even legal action. It’s a structured process designed to trace responsibility and recoup funds. The specific details can vary based on the type of insurance (auto, home, health, etc.) and the laws in your state, but the core principle remains the same: follow the money to the responsible party! It can feel a bit like a detective story, all to ensure fairness.

Subrogation in Action: A Quick Story

I remember a friend of mine, Sarah, had a fantastic vacation planned. She’d booked a non-refundable tour package months in advance. Sadly, just a week before her trip, the tour company unexpectedly declared bankruptcy and canceled all their tours. Sarah was devastated, not just about missing her dream vacation but also about losing the significant amount she’d paid. She contacted her travel insurance provider, and guess what? They assessed the situation, confirmed it was a covered loss due to the tour operator’s failure, and paid Sarah back her full costs! Then, her insurance company, using subrogation, went after the defunct tour company’s assets to try and recover some of that money. Sarah got her refund, and the insurer took on the task of trying to recoup their payout. It was a perfect illustration of subrogation working to protect the policyholder and hold the responsible party accountable, even in a tough situation. It really highlights how these policies have your back!

“Subrogation is a fundamental principle that safeguards both policyholders and the insurance system by ensuring accountability and promoting fairness. It’s a powerful tool for justice!”

Common Myths About Subrogation Busted!

Let’s clear up some common misunderstandings. A frequent myth is that subrogation means you’ll somehow have to pay your insurer back in addition to receiving your claim payout. That’s just not how it works! Your insurer pays you first. Then, *they* pursue the at-fault party. You don’t double-dip, and you don’t pay your insurer back out of your own pocket for the claim they already settled. Another myth is that subrogation applies in every single claim. This isn’t true. It only applies when a third party is legally responsible for your loss. If the loss was solely due to an ‘Act of God’ with no human negligence involved, subrogation typically wouldn’t apply. Understanding these nuances helps demystify the process and keeps things clear for you!

Myth vs. Reality: Subrogation Explained

Myth

I have to pay my insurer back for the claim I received.

Reality

Your insurer recovers funds from the at-fault party; you don’t pay them back from your own pocket for the settled claim.

Myth

Subrogation applies to every single insurance claim.

Reality

It only applies when a negligent third party is responsible for the loss.

Your Role in the Subrogation Process

While your insurance company handles the heavy lifting of subrogation, your cooperation is often key! You might be asked to provide documentation, sign certain forms (like a “Notice of Subrogation” or an “Assignment of Rights”), and be available to answer questions. It’s really important to be truthful and forthcoming. Remember, your insurance policy is a contract, and it usually grants your insurer these subrogation rights. By cooperating, you’re not just helping your insurer; you’re helping to ensure the integrity of the insurance system and potentially contributing to lower future premiums for everyone. It’s a team effort, really! Your input is valuable, so don’t hesitate to communicate.

Tips for Navigating Subrogation

- Read Your Policy: Familiarize yourself with the subrogation clause in your insurance contract. Knowing what’s in there is the first step!

- Be Honest and Cooperative: Provide accurate information and necessary documents to your insurer. Transparency builds trust.

- Don’t Sign Away Rights: Be cautious about signing any release or settlement documents from the at-fault party or their insurer without consulting your own insurer first. You might inadvertently give up your insurer’s subrogation rights! This is a big one.

- Ask Questions: If you’re unsure about any part of the subrogation process, don’t hesitate to ask your insurance adjuster or agent for clarification. They’re there to help! Clear communication is essential.

Wrapping It All Up

So there you have it! Subrogation might sound like a complex legal term, but at its heart, it’s a principle of fairness and accountability. It ensures that the party who caused the loss ultimately pays for it, and it plays a vital role in keeping insurance affordable for all of us. Knowing about subrogation empowers you as a policyholder and gives you a clearer picture of how your insurance works after a claim. It’s a win-win scenario, really, protecting you and strengthening the entire insurance community. Wasn’t that easier to understand than you thought? I sure hope so! You’ve navigated a bit of insurance legalese and come out smarter on the other side!

Frequently Asked Questions About Subrogation

Will subrogation affect my insurance premium?

Generally, subrogation itself doesn’t directly increase your individual premium. However, by helping insurers recover costs, it contributes to the overall stability and potential affordability of insurance premiums for everyone in the long run. It’s a system-wide benefit!

What if I settle with the at-fault party before my insurer pays my claim?

This is where you need to be careful! If you settle with the at-fault party and sign a release, you might be waiving your insurer’s right to subrogate. This could potentially jeopardize your own claim payout. Always consult your insurer before agreeing to any settlement with a third party.

Does subrogation always result in the at-fault party paying?

Not always. While subrogation aims to recover damages, the success depends on the specific circumstances, the evidence available, and the at-fault party’s ability to pay. Sometimes, legal action might not be feasible or cost-effective.

Can my health insurance company subrogate after I receive medical treatment?

Yes! If your injury was caused by someone else’s negligence (like in a car accident), your health insurer often has the right to subrogate against the at-fault party to recover the medical expenses they paid on your behalf. This is common in health, auto, and workers’ compensation insurance.

What happens if I have collision coverage and the other party is at fault?

If the other driver was at fault, your insurer will likely pay for your repairs under your collision coverage (minus your deductible) and then subrogate against the at-fault driver’s insurance to recover those costs, including your deductible. If they’re successful, you should get your deductible back!